Sequencing risk is the risk of experiencing poor investment performance at the wrong time, typically when an investment portfolio balance is at its greatest.

Sequencing risk is particularly important during the later part of the accumulation phase in superannuation and is particularly pertinent to Pre and Post Retirees.

Sequencing risk is an ever-present part of our superannuation system

Our superannuation system is based on Australians building up a nest egg during our working life and then drawing down on it in our retirement. For early accumulators, when the level of savings is small, maximising returns matter the most as you are able to weather market volatility in the long term. However, as your savings grow larger and as you approach retirement, there is a greater focus on the short-term because a period of un-favourable market conditions may lead to a financial retirement outcome that is not what you may have been expecting. If you experience poor investment returns around your retirement your portfolio may not have enough time to recover even if the market does eventually rebound. The risk of experiencing poor investment returns at the wrong time is called sequencing risk.

Sequencing risk is one of the biggest financial risks faced by retirees because it is a major cause of longevity risk: the risk of outliving one’s savings. If this risk is not managed properly it may lead to dramatically different retirement outcomes even if two investors are exposed to the same average return.

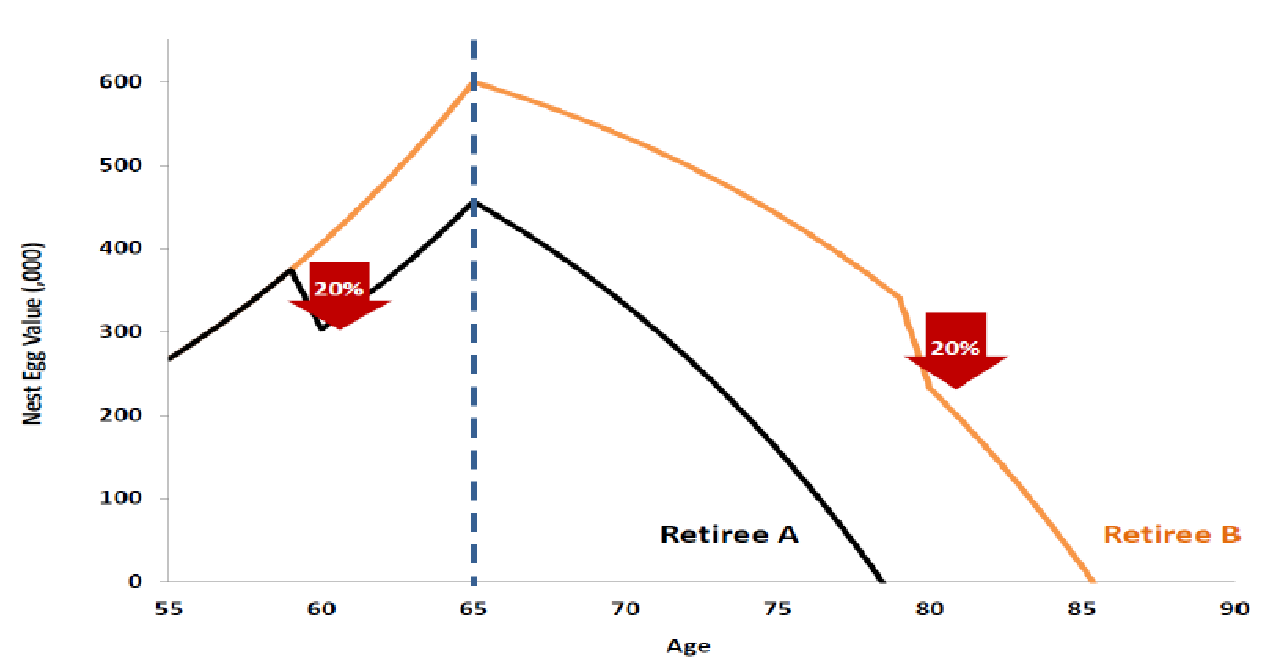

To explain further:

Consider two retirees Albert and Brian who both contribute $5,000 annually to their nest egg before retirement and then withdraw $50,000 annually when they retire from 65 years of age. Both are exposed to investment returns of 7% per annum, however, the only difference is that Albert experiences an unexpected 20% loss five years before retirement (60 years old) while Brian experiences the same percentage loss fifteen years after retirement (80 years old).

The above chart shows that if you experience a significant loss when the nest egg is large it may wipe out several years of your retirement savings.

Albert experienced a large loss before retirement and consequently increased the probability of outliving their savings. On the other hand, Brian did not experience a similar result because the loss occurred later in retirement.

Ten years ago, a well-known research report was released by Professors Doran,

Drew and Walk (2012) investigated how sequencing risk affects retirement savings and comment and concluded that:

“… a poorly timed negative return event (of around -20 per cent) can raise the probability of outliving retirement savings from 33 per cent to 50 per cent.”

The Retirement Risk Zone

Sequencing risk increases when there is more capital at risk when you approach retirement. An investment loss occurring when the nest egg is large will have a disproportionate impact on how long your savings will last.

accumulation phase as well as post-retirees in the drawdown phase. This phase of the savings life cycle is commonly called the ‘Retirement Risk Zone’. Research by Milevsky and Salisbury (2006) and Doran, Drew and Walk (2012) show that this zone spans from about 15 years before you retire to about 10 years after you retire.

The Retirement Risk Zone has High Sequencing Risk

It’s harder to make back money

The situation is much different for the younger ones

What if you are able to wait many years and let future returns offset past losses? This situation works well for young accumulators when time is on their side and when there are no cash flow withdrawals from their savings.

For post-retirees, being patient does not work because of the constant withdrawals to fund ongoing retirement expenses. Even if two retirees with the same withdrawals are exposed to the same return over the long term, different levels of volatility may again lead to dramatically different retirement outcomes.

Let us again consider Albert and Brian who retire at 65 years of age with $600,000 in savings. Both withdraw $50,000 annually to meet their retirement expenses and are exposed to a 7% per annum return over the long term. The only difference is that because of the way Albert invests his money he experiences high levels of volatility -25% in the first year and then followed by +33% to recover the loss while Brian experiences low levels of volatility -10% return in the first year and then followed by +11% to recover the loss.

‘Investor returns’ are more relevant to retirees because the constant withdrawals in times of high market volatility may lead to unsatisfactory outcomes.

Are there any solutions?

Retirees can hope to retire when the markets are rising, but hope is not a strategy to a successful retirement. There are a number of solutions a financial adviser can consider to manage sequencing risk. One strategy is that retirees can adjust their retirement spending if their savings dramatically fall in value.

However, this is a reactive strategy and it is not very useful when living and medical expenses are increasing year after year. Prevention is the best cure for the problem; accordingly, a proactive strategy is required for retirement savings.

Young savers should contribute more into their superannuation and build a larger nest egg to withstand any volatility when they approach retirement.

However, a different strategy is required for older savers within the Retirement Risk Zone. Sequencing risk should be addressed before retirement as part of a transition strategy from the accumulation phase to the drawdown phase. Unfortunately, sequencing risk can never be eliminated because returns are unpredictable; however, its effects can be managed by minimising volatility. Returns that are less volatile will have smaller negative returns.

One strategy a financial adviser could adopt is to recommend increasing the portfolio exposure of low-risk assets such as fixed interest as a client approaches retirement. However, greater exposure to fixed interest products, especially when interest rates have been low for so long and with fixed interest investments reporting a decreased capital value, it is very unlikely in today’s rising inflation environment to keep pace with increasing living costs. This strategy will result in a retiree drawing down their savings even faster than expected and consequently accelerating the risk of outliving their retirement savings.

At this current point in time retirees (and their advisers) are currently “trapped between a rock and a hard place” when considering an optimal mix between growth and defensive assets. A high allocation to fixed interest reduces sequencing risk, but it will unlikely match rising living costs leading to greater withdrawals from savings. On the other hand, a high allocation to shares will provide a good inflation hedge but the extreme volatility with constant withdrawals may not see the nest egg doing so well.

It is important to realise that retirees aim to maximise ‘investor returns’ not ‘investment returns’, so outperforming in down markets is far more important than underperforming in up markets. It takes more effort to regain lost capital especially when the capital is drawn down in unfavourable market environments.

What about employing a dynamic asset allocation strategy?

They believe that there is a greater chance of a successful outcome for a retiree even if the retiree experiences an unfavourable market environment early because a rising allocation to shares through time will maximise their exposure when the market rebounds.

Summary

And so, the key message is: Seek Advice

Sources:

Jason Teh Senior Portfolio Manager (IML Equity Income Fund) Sequencing Risk: Pre-and Post-Retiree dilemma.

Ang, A., Chen, B., Sundaresan, S., 2013, Liability-Driven Investment with Downside Risk, Journal of Portfolio Management,

Vol. 40, No. 1, pp. 71-87.

Basu, A., Byrne, A. and Drew, M., 2011, Dynamic Lifecycle Strategies for Target Date Retirement Funds, Journal of Portfolio

Management, Vol. 37, No. 2, pp. 83-96.

Doran, B., Drew, M., Walk, A., 2012, The Retirement Risk Zone: A Baseline Study, JASSA – Issue 1 2012, Financial Services

Institute of Australasia.

Milevsky, M. and Salisbury, T., 2006, Asset Allocation and the Transition to Income: The Importance of Product Allocation in

the Retirement Risk Zone, working paper, York University. Available at

http://www.ifid.ca/pdf_workingpapers/WP2006OVT3.pdf

Pfau, W. and Kitces, M., 2013, Reducing Retirement Risk with a Rising Equity Glide-Path. Available at SSRN:

http://dx.doi.org/10.2139/ssrn.2324930